Evonsys is propelling industries into the future, transforming operations and customer experiences with low-code solutions that unlock unprecedented levels of efficiency and innovation.

Since 2015, Evonsys has harnessed the power of low code to refine global organizations. We've revolutionized sectors from banking to retail with our comprehensive solutions, focusing on risk mitigation, management optimization, and streamlined automation for unrivaled efficiency.

ISO 20022 and the New Era of Domestic Payment Investigations

Posted by

ISO 20022 has been around since 2004, and while it’s taken nearly two decades to gain real traction in cross-border and high-value payments,

ISO 20022 has been around since 2004, and while it’s taken nearly two decades to gain real traction in cross-border and high-value payments, its impact is clear now. The next question is: what does this mean for domestic payments?

Real-time and instant payment schemes are expanding rapidly across major markets, gradually replacing legacy systems. Banks are processing millions of domestic transactions every day, from retail transfers to high-value corporate payments, and investigations can't afford to be slow, fragmented, or prone to errors. Today, payments need to be tracked, analyzed, and resolved quickly, and ISO 20022 helps enable faster, more consistent handling.

It’s easy to think of ISO 20022 as just a messaging upgrade, but it’s much more than that for domestic payments. It organizes payment data, standardizes how information is captured and shared, and makes exception handling far more manageable.

For banks, this means failed or disputed payments can be traced and resolved faster, workflows are smoother, and manual errors drop significantly. In short, ISO 20022 is transforming how banks operate daily and paving the way for a new era of domestic payment investigations.

Why ISO 20022 matters for domestic payments now

Domestic payment systems are scaling at an unprecedented pace. According to ACI Worldwide’s 2024 report, the world processed around 266 billion real time transactions in 2023 with a major share coming from domestic rails.

The United States has seen rapid progress. FedNow was built on ISO 20022 from day one and continues to expand. The RTP Network also supports ISO 20022 messages. The biggest shift came in July 2025 when the Fedwire Funds Service completed its migration to ISO 20022. This brought high value domestic payments into alignment with global standards. It also unlocked richer data, better automation, and improved alignment between domestic and cross border rails.

In Europe, the T2 platform replaced TARGET2 and now operates fully on ISO 20022. SEPA schemes also rely on ISO 20022, although each market follows its own rules. The United Kingdom has transitioned both CHAPS and RTGS to ISO 20022. Enhanced data rules are planned for 2027. These changes will bring greater clarity, accuracy, and deeper consistency across domestic investigations.

Asia is also moving fast. India’s UPI ecosystem continues to scale with structured identifiers and metadata. Singapore’s PayNow and Australia’s NPP use ISO 20022 aligned formats for richer messaging and smoother exception handling.

All of these systems share one common theme. Structured data creates the foundation for better investigations and a more intelligent case lifecycle.

The Earlier Challenges That Slowed Domestic Investigations

Domestic payments often appear simple on the surface, but in reality, they involve multiple systems, validations, and checks. Legacy domestic payment formats and processes created a series of operational and data-related challenges that slowed investigations and increased risk. Some of the most significant issues include:

Unstructured or incomplete payment data

Traditional domestic formats often lacked enforced structure, resulting in transactions missing critical fields such as payer and payee details, account references, or remittance information. Investigators had to manually interpret or request missing data, which increased processing time and risk of error.

Insufficient identifiers for remittance matching

Many domestic payment systems did not provide unique end-to-end references or standardized invoice identifiers. This made reconciliation difficult, especially when multiple payments were processed for the same customer or invoice. Manual intervention was often required to match transactions correctly.

Inconsistent reason codes and status indicators

Payment exceptions or rejections were often recorded differently across banks and systems. Two identical exceptions could carry different codes, forcing investigators to decode and cross-reference them manually, adding complexity and increasing resolution time.

Limited traceability across payment hops

Domestic payments frequently traverse multiple internal systems, clearinghouses, and settlement engines. Legacy formats did not capture end-to-end lifecycle data, leaving blind spots that slowed the identification of failed or delayed transactions.

Fragmented operational workflows

Investigations were often managed across disconnected platforms, spreadsheets, or bespoke tools. This led to duplicated work, lost context, and extended resolution timelines.

Heavy reliance on manual interbank follow-ups

When information was incomplete or unclear, investigators relied on phone calls, emails, or internal messaging to clarify payment details. This was slow, prone to human error, and incompatible with high-volume real-time payments.

Pressure from real-time and instant payment rails

Modern domestic payment systems including, RTP in the United States Faster Payments in the UK, SEPA Instant in Europe, UPI in India and PayNow in Singapore process transactions within seconds. This means any failed or disputed payment must be identified and resolved almost immediately. Traditional manual processes cannot keep up, leaving banks exposed to operational and customer risk.

How ISO 20022 Transforms Domestic Payment Investigations

ISO 20022 is reshaping domestic payments by providing a consistent, structured, and enriched data standard. It allows banks to move from slow, reactive investigations to faster, automated, and more efficient operations. Here’s how it makes a difference:

Structured and enriched payment data

Every ISO 20022 message comes with clearly defined fields for payer, payee, and transaction details. Investigators no longer need to manually interpret incomplete information. The standardized data also allows banks to automate reconciliation, reducing errors and accelerating the resolution of exceptions.

Smarter remittance and reconciliation

With detailed creditor and debtor information, invoice references, and remittance advice included in every transaction, banks can automatically match payments across accounts and systems. This capability significantly reduces manual work and improves accuracy, even when processing millions of domestic transactions each day.

Consistent reason codes and exception reporting

ISO 20022 introduces standard code lists that schemes can adopt to make exceptions more consistent. This standardization simplifies root-cause analysis and ensures that payment issues are handled consistently across banks and systems, reducing confusion and speeding up investigations.

Full traceability across payment hops

Domestic payments often pass through multiple internal systems, clearinghouses, and instant payment rails. ISO 20022 captures end-to-end transaction details, giving investigators complete visibility into every step. This traceability allows banks to identify and resolve issues faster without relying on fragmented manual processes.

Streamlined workflows across platforms

Standardized data enables banks to harmonize investigation processes across multiple systems. Operations teams can collaborate more effectively, reduce duplicated work, and create predictable resolution workflows that scale with high-volume domestic payment environments.

Automation and real-time readiness

The structured and enriched data ISO 20022 provides allows banks to implement automated monitoring and AI-assisted exception handling. Investigators can quickly identify failed or disputed payments and route them for resolution in near real-time, keeping pace with fast-moving domestic rails like RTP, UPI, Faster Payments, SEPA Instant, and PayNow.

Operational efficiency and cost reduction

By reducing manual interventions and errors, ISO 20022 enables faster exception resolution and lowers operational costs. Banks can process higher volumes of payments without adding proportional resources, while also improving the overall reliability and predictability of investigations.

Support for predictive analytics and advanced monitoring

With standardized, enriched data available across all transactions, banks can build predictive models, early warning systems, and advanced analytics. This allows potential exceptions to be identified proactively, improving operational resilience and ensuring better customer experience in real-time payment environments.

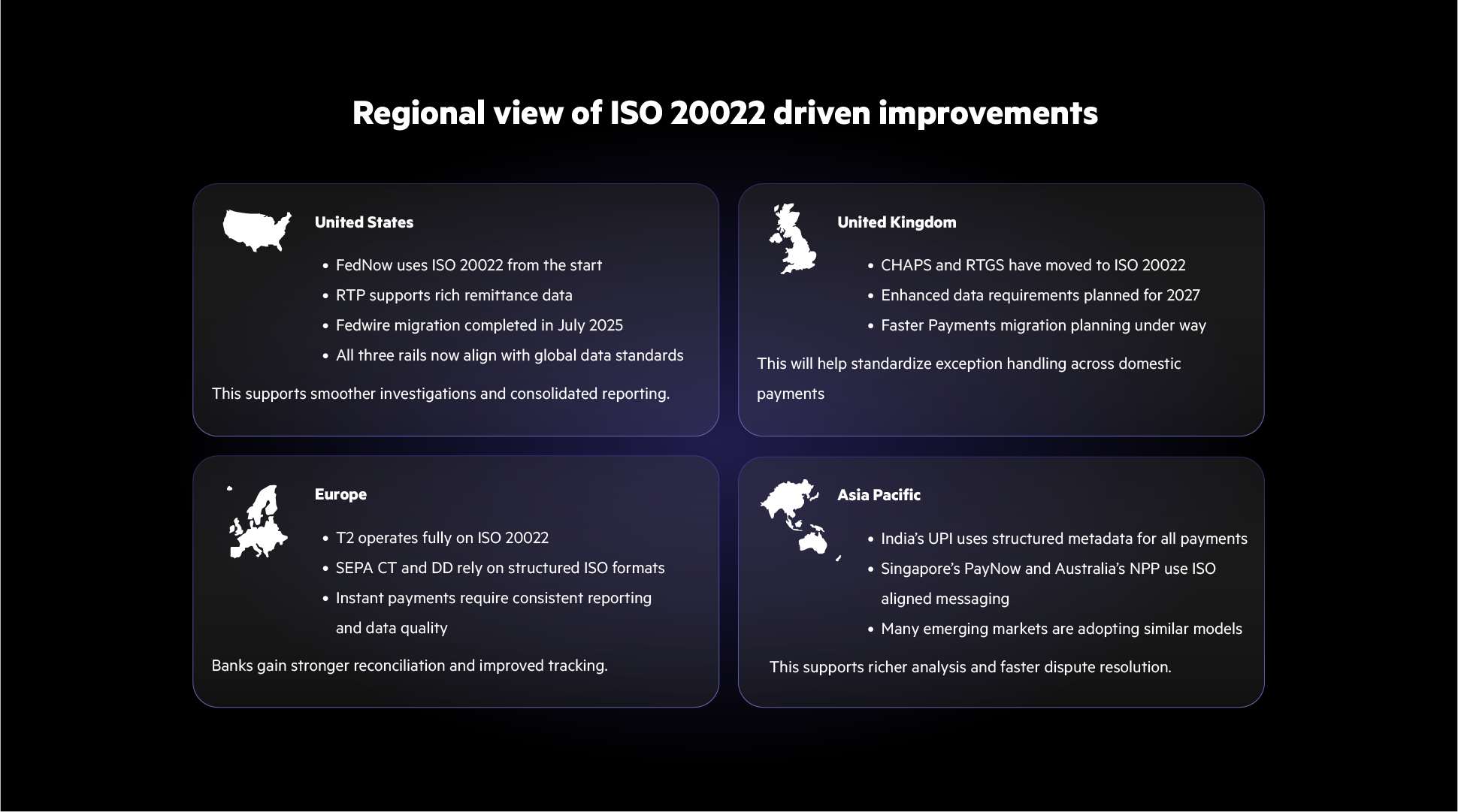

Regional view of ISO 20022 driven improvements

United States

FedNow uses ISO 20022 from the start

RTP supports rich remittance data

Fedwire migration completed in July 2025

All three rails now align with global data standards

This supports smoother investigations and consolidated reporting.

United Kingdom

CHAPS and RTGS have moved to ISO 20022

Enhanced data requirements planned for 2027

Faster Payments migration planning under way

This will help standardize exception handling across domestic payments.

Europe

T2 operates fully on ISO 20022

SEPA CT and DD rely on structured ISO formats

Instant payments require consistent reporting and data quality

Banks gain stronger reconciliation and improved tracking.

Asia Pacific

India’s UPI uses structured metadata for all payments

Singapore’s PayNow and Australia’s NPP use ISO aligned messaging

Many emerging markets are adopting similar models

This supports richer analysis and faster dispute resolution.

The future of domestic investigations

ISO 20022 gives domestic payment teams the structured and enriched data they need to handle investigations with more clarity and speed. As real-time payment schemes continue to grow, this consistency becomes essential.

Banks can trace issues more easily, automate parts of the investigation flow, and reduce the manual friction that once slowed domestic operations. The result is faster identification of errors and a more predictable investigation process across high-volume domestic channels.

Please fill out this form to get in touch with us. The information you provide regarding your requirement will help us reach out to you with the best solution.

Unit 18, 23 Veron Street Wentworthville, Sydney 2145, Australia +61 (02) 8006 0032

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

ISO 20022 has been around since 2004, and while it’s taken nearly two decades to gain real traction in cross-border and high-value payments, its impact is clear now. The next question is: what does this mean for domestic payments?

Real-time and instant payment schemes are expanding rapidly across major markets, gradually replacing legacy systems. Banks are processing millions of domestic transactions every day, from retail transfers to high-value corporate payments, and investigations can't afford to be slow, fragmented, or prone to errors. Today, payments need to be tracked, analyzed, and resolved quickly, and ISO 20022 helps enable faster, more consistent handling.

It’s easy to think of ISO 20022 as just a messaging upgrade, but it’s much more than that for domestic payments. It organizes payment data, standardizes how information is captured and shared, and makes exception handling far more manageable.

For banks, this means failed or disputed payments can be traced and resolved faster, workflows are smoother, and manual errors drop significantly. In short, ISO 20022 is transforming how banks operate daily and paving the way for a new era of domestic payment investigations.

Why ISO 20022 matters for domestic payments now

Domestic payment systems are scaling at an unprecedented pace. According to ACI Worldwide’s 2024 report, the world processed around 266 billion real time transactions in 2023 with a major share coming from domestic rails.

The United States has seen rapid progress. FedNow was built on ISO 20022 from day one and continues to expand. The RTP Network also supports ISO 20022 messages. The biggest shift came in July 2025 when the Fedwire Funds Service completed its migration to ISO 20022. This brought high value domestic payments into alignment with global standards. It also unlocked richer data, better automation, and improved alignment between domestic and cross border rails.

In Europe, the T2 platform replaced TARGET2 and now operates fully on ISO 20022. SEPA schemes also rely on ISO 20022, although each market follows its own rules. The United Kingdom has transitioned both CHAPS and RTGS to ISO 20022. Enhanced data rules are planned for 2027. These changes will bring greater clarity, accuracy, and deeper consistency across domestic investigations.

Asia is also moving fast. India’s UPI ecosystem continues to scale with structured identifiers and metadata. Singapore’s PayNow and Australia’s NPP use ISO 20022 aligned formats for richer messaging and smoother exception handling.

All of these systems share one common theme. Structured data creates the foundation for better investigations and a more intelligent case lifecycle.

The Earlier Challenges That Slowed Domestic Investigations

Domestic payments often appear simple on the surface, but in reality, they involve multiple systems, validations, and checks. Legacy domestic payment formats and processes created a series of operational and data-related challenges that slowed investigations and increased risk. Some of the most significant issues include:

Unstructured or incomplete payment data

Traditional domestic formats often lacked enforced structure, resulting in transactions missing critical fields such as payer and payee details, account references, or remittance information. Investigators had to manually interpret or request missing data, which increased processing time and risk of error.

Insufficient identifiers for remittance matching

Many domestic payment systems did not provide unique end-to-end references or standardized invoice identifiers. This made reconciliation difficult, especially when multiple payments were processed for the same customer or invoice. Manual intervention was often required to match transactions correctly.

Inconsistent reason codes and status indicators

Payment exceptions or rejections were often recorded differently across banks and systems. Two identical exceptions could carry different codes, forcing investigators to decode and cross-reference them manually, adding complexity and increasing resolution time.

Limited traceability across payment hops

Domestic payments frequently traverse multiple internal systems, clearinghouses, and settlement engines. Legacy formats did not capture end-to-end lifecycle data, leaving blind spots that slowed the identification of failed or delayed transactions.

Fragmented operational workflows

Investigations were often managed across disconnected platforms, spreadsheets, or bespoke tools. This led to duplicated work, lost context, and extended resolution timelines.

Heavy reliance on manual interbank follow-ups

When information was incomplete or unclear, investigators relied on phone calls, emails, or internal messaging to clarify payment details. This was slow, prone to human error, and incompatible with high-volume real-time payments.

Pressure from real-time and instant payment rails

Modern domestic payment systems including, RTP in the United States Faster Payments in the UK, SEPA Instant in Europe, UPI in India and PayNow in Singapore process transactions within seconds. This means any failed or disputed payment must be identified and resolved almost immediately. Traditional manual processes cannot keep up, leaving banks exposed to operational and customer risk.

How ISO 20022 Transforms Domestic Payment Investigations

ISO 20022 is reshaping domestic payments by providing a consistent, structured, and enriched data standard. It allows banks to move from slow, reactive investigations to faster, automated, and more efficient operations. Here’s how it makes a difference:

Structured and enriched payment data

Every ISO 20022 message comes with clearly defined fields for payer, payee, and transaction details. Investigators no longer need to manually interpret incomplete information. The standardized data also allows banks to automate reconciliation, reducing errors and accelerating the resolution of exceptions.

Smarter remittance and reconciliation

With detailed creditor and debtor information, invoice references, and remittance advice included in every transaction, banks can automatically match payments across accounts and systems. This capability significantly reduces manual work and improves accuracy, even when processing millions of domestic transactions each day.

Consistent reason codes and exception reporting

ISO 20022 introduces standard code lists that schemes can adopt to make exceptions more consistent. This standardization simplifies root-cause analysis and ensures that payment issues are handled consistently across banks and systems, reducing confusion and speeding up investigations.

Full traceability across payment hops

Domestic payments often pass through multiple internal systems, clearinghouses, and instant payment rails. ISO 20022 captures end-to-end transaction details, giving investigators complete visibility into every step. This traceability allows banks to identify and resolve issues faster without relying on fragmented manual processes.

Streamlined workflows across platforms

Standardized data enables banks to harmonize investigation processes across multiple systems. Operations teams can collaborate more effectively, reduce duplicated work, and create predictable resolution workflows that scale with high-volume domestic payment environments.

Automation and real-time readiness

The structured and enriched data ISO 20022 provides allows banks to implement automated monitoring and AI-assisted exception handling. Investigators can quickly identify failed or disputed payments and route them for resolution in near real-time, keeping pace with fast-moving domestic rails like RTP, UPI, Faster Payments, SEPA Instant, and PayNow.

Operational efficiency and cost reduction

By reducing manual interventions and errors, ISO 20022 enables faster exception resolution and lowers operational costs. Banks can process higher volumes of payments without adding proportional resources, while also improving the overall reliability and predictability of investigations.

Support for predictive analytics and advanced monitoring

With standardized, enriched data available across all transactions, banks can build predictive models, early warning systems, and advanced analytics. This allows potential exceptions to be identified proactively, improving operational resilience and ensuring better customer experience in real-time payment environments.

Regional view of ISO 20022 driven improvements

United States

FedNow uses ISO 20022 from the start

RTP supports rich remittance data

Fedwire migration completed in July 2025

All three rails now align with global data standards

This supports smoother investigations and consolidated reporting.

United Kingdom

CHAPS and RTGS have moved to ISO 20022

Enhanced data requirements planned for 2027

Faster Payments migration planning under way

This will help standardize exception handling across domestic payments.

Europe

T2 operates fully on ISO 20022

SEPA CT and DD rely on structured ISO formats

Instant payments require consistent reporting and data quality

Banks gain stronger reconciliation and improved tracking.

Asia Pacific

India’s UPI uses structured metadata for all payments

Singapore’s PayNow and Australia’s NPP use ISO aligned messaging

Many emerging markets are adopting similar models

This supports richer analysis and faster dispute resolution.

The future of domestic investigations

ISO 20022 gives domestic payment teams the structured and enriched data they need to handle investigations with more clarity and speed. As real-time payment schemes continue to grow, this consistency becomes essential.

Banks can trace issues more easily, automate parts of the investigation flow, and reduce the manual friction that once slowed domestic operations. The result is faster identification of errors and a more predictable investigation process across high-volume domestic channels.

_New_3%20(1).jpg)

_New_8.jpg)

.png)

.png)