Evonsys is propelling industries into the future, transforming operations and customer experiences with low-code solutions that unlock unprecedented levels of efficiency and innovation.

Since 2015, Evonsys has harnessed the power of low code to refine global organizations. We've revolutionized sectors from banking to retail with our comprehensive solutions, focusing on risk mitigation, management optimization, and streamlined automation for unrivaled efficiency.

Extending E&I Into the Front Office: Turning a Back Office Function into a Customer Advantage

Extending E&I Into the Front Office: Turning a Back Office Function into a Customer Advantage

December 5, 2025

HIGHLIGHTS

ON THIS PAGE

For years, every bank has treated Exceptions and Investigations as something that lives far away from customers.

It sits deep inside the back office, handled by specialists, surrounded by legacy workflows, and largely disconnected from the teams who actually face clients.

That model made sense when payments moved slowly, and customers were willing to wait.

Yes, today clients expect real-time answers, clear visibility, and zero friction.

Corporate treasurers want immediate clarity on high value payments.

Retail customers expect instant updates on transfers.

Relationship Managers and call center teams need live information to maintain trust at the moment.

And regulators expect banks to demonstrate traceability and control across the entire payment flow.

The reality is clear. E&I is no longer a back-office function. It is becoming a core part of the customer experience.

If banks keep it hidden, they lose an opportunity to strengthen customer relationships, reduce operational load, and differentiate themselves in the market from competitors.

This is the moment to bring E&I into the front office.

Why E&I Needs to Move Out of the Back Office

Most banks still run payment investigations using a 20-year-old playbook.

Whenever a customer asks, “Where is my payment?”

The front office captures the query and forwards it to operations.

The operations team pulls information from different systems, checks with specialists, traces the payment manually, and eventually sends an update back.

By the time the answer reaches the customer, the moment of trust has already vanished, and the bank has invested more effort than necessary.

This old model creates delays because the front office has:

Limited visibility, and the operations team relies heavily on individual expertise, siloed systems, and manual interpretation

Also, this process is slow, reactive, and increasingly misaligned with real-time customer expectations.

When E&I becomes visible across the bank, the entire experience transforms:

Front office teams gain real time visibility

Your relationship managers and customer service representatives become capable of answering questions on the spot. They can initiate a real time inquiry, see where the payment is stuck, understand which bank is holding it, and know immediately whether it’s a compliance check, a missing detail, or a delay at an intermediary.

They can initiate a structured inquiry, track the response, and give the customer an informed update—all within the same conversation. No emails. No callbacks. No handoffs.

Customers get transparency at the exact moment they need it

Customers have long been able to track a courier package in real time, seeing every scan and knowing exactly when it will arrive. Payments are now just as traceable thanks to Swift GPI. A Unique End-to-End Transaction Reference (UETR) is a single, unique identifier which acts like a tracking number and allows anyone involved in the payment chain to know the exact status of a payment, including where it is and when it was ultimately credited to the beneficiary.

APIs provide instant access to this information. Therefore, it is essential to make these APIs available across all your customer-facing digital channels, enabling customers to self-serve and have real-time insight and traceability into their payments.

Whether they call the help desk, walk into a branch, log into a treasury portal, or open a mobile app, customers get a real-time view of what’s happening with their payment. There’s no waiting for someone to “check internally” or call back later. The information they need is already available at the exact moment they need it and what’s more, it can be bi-directional. If an overseas bank has a question about a payment initiated by your customer, they can use the same digital channels to relay the request to your customer for their information or action.

Self-service becomes possible at scale

As soon as the underlying data and case workflows are connected, self-service becomes easy to deliver. Customers can conduct an investigation on their own, track its progress, understand the reason for delays, and receive updates instantly.

Automation is what makes this front-office, self-service idea possible. This automation is driven by ISO 20022 and Swift Case Orchestrator in the background, which defines the rulebook and communication mechanisms. If a customer wants to chase a payment, or they are unsure what a credit is for, or why a $25 charge was deducted, the underlying message types and business rules determine exactly how each investigation type is executed.

Exposing that E&I business process to an email channel, CRM, or front-office digital channel allows any initiating channel to invoke an automated E&I workflow that is already defined and operational in the back-office system. This reduces unnecessary pressure on specialists, who no longer need to handle simple trace requests, and it gives customers confidence by making the process visible and responsive.

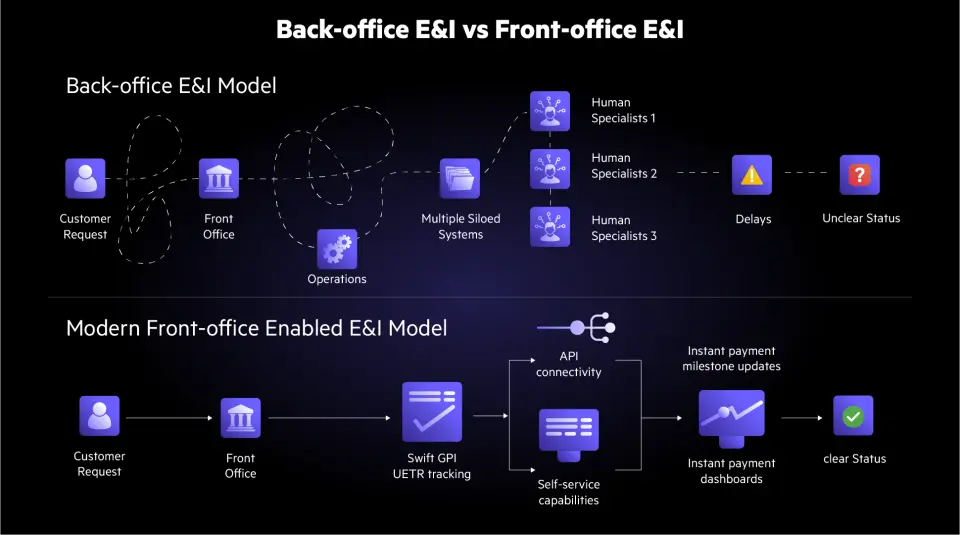

The Connected E&I Ecosystem: Front Office Vs Back Office

Traditional back-office E&I follows sequential, manual case handling, while front-office E&I uses real-time data to respond instantly and keep clients informed. This contrast is shown in the diagram below:

Why This Shift Is Urgent

Banks are being pushed to modernize exception handling much faster than before. Several industry dynamics are increasing the pressure and making front-office enabled investigations unavoidable.

Instant payment rails are leaving no room for delay

With the rise of RTP, FedNow, SEPA Instant, UPI, and real-time cross-border services like Swift GPI and Swift Transaction Manager, customers now expect payments to clear in seconds. When payments move this fast, any delay feels unacceptable. If a payment is instant, the investigation must start instantly as well.

Real-time payment rails also generate continuous event data such as end-to-end references, GPI UETRs, and ISO 20022 status updates. If the front office cannot see this data in real time, even small delays become visible to customers and quickly erode trust.

Customer expectations are being shaped by other industries

Treasury teams now expect the same level of visibility they get from logistics platforms which show live shipment scans or freight milestones. They expect to see intermediary bank hops, timestamps, pacs.002 status codes, and investigation triggers as soon as they occur.

Retail customers expect immediate notifications when a payment fails screening, hits a repair queue, or awaits beneficiary bank confirmation. If other apps can show location, status, and next steps, customers expect banking to match that level of transparency.

Operational pressure is growing continuously

Payment volumes are rising, and each payment now carries more structured data, more compliance checks, and more cross-border dependencies. With ISO 20022 migration, banks handle richer fields, larger payloads, and more nuanced error codes. This increases the number of investigation triggers.

Manual investigations cannot scale with this volume. Case queues grow, internal SLAs slip, and specialists spend too much time handling basic traces instead of resolving complex exceptions. When the front office does not have access to real time data or case orchestration, the number of escalations multiplies and operational cost rises sharply.

Rising Operational Risks from Sanctions and Geopolitics

Geopolitical uncertainty and tightening global sanctions create additional friction in the payment lifecycle. Sanction hits can stop payments mid-flow, immediately increasing E&I volume and affecting customer satisfaction. Banks must provide transparent updates and clear explanations whenever these holds occur.

Without real-time data or access to case orchestration in the front office, escalations multiply, operational costs rise sharply, and the customer experience suffers.

The Industry Breakthroughs That Make Front-Office E&I a Reality Today

The shift towards front-office enabled E&I is now possible because multiple innovations have converged. ISO 20022 provides structured, standardized messages that eliminate ambiguity, while Swift Case Orchestrator acts as the central brain, routing investigations automatically and applying the correct business rules.

Swift GPI and Transaction Manager deliver a UETR tracking number for each payment, giving instant visibility into its status, intermediary banks, and compliance checks. With these capabilities, inquiries can be initiated from mobile apps, portals, call centers, or relationship manager desktops, and the system executes the investigation automatically, providing immediate answers.

Stop and Recall operations enhance this model by proactively intercepting payments that may cause exceptions, reduce manual investigation volume, and allowing front-office teams to respond to customers in real time.

Five years ago, these capabilities were fragmented and incomplete. Today, their integration allows banks to surface actionable, real-time insights to both customers and staff, transforming E&I from a hidden back-office process into a strategic, customer-facing function that builds trust, improves operational efficiency, and strengthens the overall customer experience.

Conclusion

Extending E&I into the front office is not simply a technology modernization. It is a strategic shift that changes how customers experience your bank.

It creates a service model built on transparency, empowerment, and real-time information. It strengthens relationships, reduces operational cost, and positions the bank for a future where speed and clarity will define competitive advantage.

Banks that make this shift early will stand out as transparent, responsive, and customer centric. Banks that delay will continue to struggle with slow response times, increased cost, and loss of trust.

The path forward is clear. Bring E&I to the places where your customers interact with you. Give your teams the tools they need to answer confidently. Build a unified orchestrated backbone. And let your customers get the clarity they deserve, exactly when they need it.

.png)

.png)

.png)

.png)