.png)

.png)

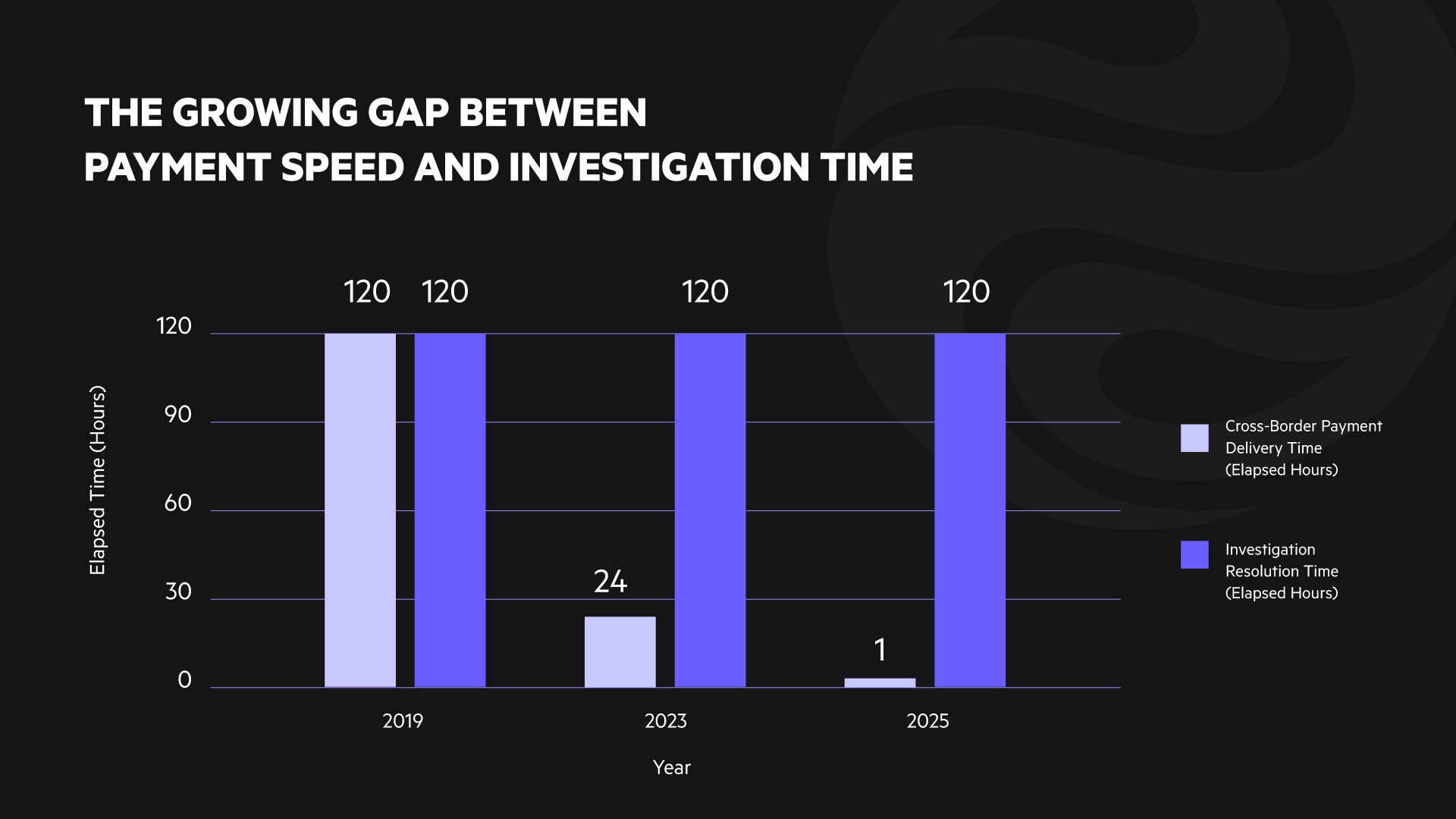

Payments are being handled quicker than ever, and cross-border payments that would have taken days are now arriving in under an hour. However, when an exception occurs, investigation could still take several days. This growing gap is something that many banks need to consider and rethink how payment investigations are managed.

The graph below shows this difference, highlighting why modernization has become more important for many financial institutions.

For many banks and financial institutions, this gap isn't just an inconvenience. It has become a competitive disadvantage. While November 2025 marks the completion of the ISO 20022 migration for cross-border payments (SR2025), it also represents the beginning of a new phase for payment investigations.

With SR2026 introducing timelines for Stop and Recall and inbound investigations, and SR2027 extending to outbound cases, the clock is now ticking for banks to modernize how payment exceptions and investigations are managed.

With ISO 20022 migrations, SWIFT’s SR2025 CBPR+ cash management message changes, and emerging regulatory expectations, now is the time to rethink how payment exceptions and investigations are handled. In this article, we:

Swift’s SR2025 represents a major shift in the way payments are exchanged. Starting November 22, 2025, all cross-border payments will migrate fully to the ISO 20022 MX format via the FINplus Service. Legacy FIN MT messages (including MT 103, MT 202, MT 205, and their variants) will no longer be supported on the Swift FIN network. Many banks will still need backup processes for those MT flows that have not fully migrated.

Once coexistence ends, any MT message which SR has not supported will produce a negative acknowledgement (NAK). In-flow translation will also become a paid service. Payments that cannot immediately migrate to MX will potentially be converted and routed using FINplus as part of the contingency process.

SR2025 introduces critical updates to payment message standards, including a new hybrid postal address model requiring structured country and town fields, with up to two unstructured address lines. Full unstructured formats will be phased out by November 2026. All messages must include a valid usage identifier in the business service field—missing or incorrect values may cause routing or validation failures.

Additionally, end-to-end traceability is now mandatory, requiring the use of UETR (Unique End-to-End Transaction Reference), Instruction ID, Msg ID, and end-to-end ID to ensure full auditability and compliance across the payment chain.

Swift is extending its support for exceptions and investigations via structured messages including camt.110 and camt.111 for CBPR+ payments. The updated case management service aims to reduce dependency on MT-based exception flows and improve turnaround time.

Also, the Stop and Recall service facilitates the cancellation of fraudulent payments by leveraging structured messages like MT192 and MT199, or their ISO 20022 equivalents, camt.055 and camt.056. This integration enables banks to quickly halt payments in progress, minimizing potential losses and enhancing operational efficiency.

The SR2025 changes and ISO 20022 migration begin the journey towards a fully modernized process for payment investigations. SR2026 and SR2027 will complete that journey as it relates to cross-border payment investigations.

MT messages have been around for over 40 years, and investigation teams are highly familiar with them. On the other hand, ISO20022 MX messages are verbose and complex, designed for system-to-system communication, not for human reading. Without automation, even experienced investigators face a steep learning curve to interpret these messages.

MX payment investigation messages are ideal for automation. Their structured format and code-driven content make machine reading much easier than the legacy MT messages. Without automation, banks will find it hard to take full advantage of the promise of ISO20022 and might even operate less efficiently than before the ISO 20022 implementation.

Cross-border payments used to take days. But now they happen in hours. Customers expect the same speed when they raise an investigation. They want answers quickly. They also want the flexibility of being able to submit requests through email, mobile, or online banking. When your competitors are going to leverage ISO 20022 to enhance their customer experience, you need to do the same to remain competitive.

Banks might assume that migrating to ISO 20022 for payment investigation messages is a one-time effort. They may expect to put it on autopilot and focus on other priorities. The reality is different.

SWIFT issues annual compliance updates through its November CBPR+ standards releases, and each domestic scheme follows its own compliance schedule, adding further complexity. The reality is that the ISO 20022 migration for E&I marks the start of the compliance journey, not the end.

Due to the changing regulations and compliance requirements, many banks encounter several challenges that make the modernization of payment investigations critical.

Many banks operate under tight budgets and limited resources. As a result, they may find it challenging to adopt ISO 20022 and implement automation systems.

Many financial organizations and banks still operate with manual workflows for investigations or utilize a spreadsheet-based structure. These methods increase human error rates resulting in missing SLA deadlines and resolution times.

Transitioning to ISO 20022 and MX messages requires staff training and skill development. Without proper upskilling, teams may struggle to interpret, process, and investigate structured messages efficiently.

Most banks usually rely on multiple third-party providers to perform payment processing, reconciliation, and case management. Coordinating all these vendors to migrate to ISO 20022 increases the risk of delays and miscommunication.

Customers expect quick and transparent payment handling, including payment exceptions and investigations. If a bank fails to meet these expectations, it might result in a decline of customers' happiness index and potentially lead to reputational damage.

All these kinds of organizational gaps can create risks of regulatory penalties, client complaints, and potential loss of business.

In essence, SR2025’s CBPR+ ISO 20022 changes are not just simple technical updates. They set new rules and standards for cross-border payments and payment investigations. For many banks, this marks the beginning of a multi-year journey with both opportunities and challenges.

As messaging standards evolve and resources remain constrained, banks may struggle to adapt. Those who embrace the trends introduced by SR2025—and plan ahead for SR2026 and SR2027—can build systems that deliver faster resolution times, and greater operational efficiency.

In more practical terms, payment investigation platforms are the gateway for ensuring industry compliance, improving customer experience, and resilience in operations. Banks that choose to act today can migrate their legacy process flows like manual or paper-based into more process-oriented workflows that are defined as a part of ISO 20022 compliance.

Secure Your Early Access to The Future of Payment Investigations

Be among the first to get started with our ISO 20022 & Swift-Ready cross-border payment investigation platform to streamline your payment exception handling.

.png)

.png)