.png)

.png)

Payment volumes are constantly rising across domestic and cross-border networks. But this rapid growth also exposes the limits of existing operational models, placing increasing pressure on banks to deliver speed, transparency, and accuracy at scale. Corporate and retail customers now expect timely answers when a payment is delayed, missing, or disputed. However, payment investigations remain one of the most operationally intensive and inefficient areas within banking.

Despite years of investment in payment modernization, many investigation workflows still rely on manual processes, fragmented data, and legacy messaging formats. Teams spend significant time gathering information, coordinating across institutions, and responding to repeated queries from customers and internal stakeholders. The result is higher operational cost, longer resolution timelines, increased compliance risk, and declining customer satisfaction.

The introduction of ISO 20022, supported by orchestration capabilities such as SWIFT Case Orchestrator, is changing how banks approach investigations. Structured, machine-readable data combined with centralized workflow orchestration enables banks to move investigations from a reactive back-office function to a more efficient, transparent, and strategic operational capability. This blog examines the challenges in the current investigations landscape, explains why ISO 20022 is a turning point, and outlines how banks, particularly mid-sized institutions, can modernize investigation workflows in a practical and scalable way and enhance their customer experience in the process.

In many banks, payment investigations still follow a manual and sequential model. When an inquiry is raised by a creditor or customer, the request moves from one institution to another through a series of handoffs. Each intermediary must review the request, search for information in internal systems, and respond before the case progresses further. This approach introduces unavoidable delays and increases the likelihood of incomplete or inconsistent responses.

Investigators often rely on multiple systems, email threads, spreadsheets, and free-text messages to reconstruct the history of a transaction. Information may be stored in legacy MT messages, domestic payment platforms, or unstructured communications that are not easily searchable. Limited automation means that repetitive and rule-based tasks continue to consume valuable staff time.

Visibility is another major challenge. Frontline teams and customers frequently have little insight into the status of an investigation, leading to repeated follow-ups and frustration. Internally, operations managers struggle to track workloads, aging cases, and SLA breaches in real time.

These inefficiencies carry measurable financial and reputational consequences. Large banks report annual costs running into tens of millions of dollars due to delayed payments, compensation claims, and operational overhead. Poor investigation experiences also contribute to corporate client churn, which directly impacts long-term revenue and trust.

ISO 20022 represents a fundamental shift in how payment data is structured and exchanged. Unlike legacy message formats that rely heavily on free-text fields, ISO 20022 uses standardized, structured, and machine-readable data elements. This allows systems to interpret and process information consistently without manual intervention.

Each payment message contains rich contextual data, including clear remittance information and consistent identifiers such as the Unique End-to-End Transaction Reference, Instruction ID, and End-to-End ID. These identifiers enable transactions to be traced and correlated across systems and institutions with far greater accuracy.

For investigations, this data richness is critical. Structured information improves reconciliation, reduces ambiguity, and makes it easier to match investigation cases to their underlying transactions. Investigators no longer need to interpret unstructured text or search across multiple systems to understand the status of a payment.

ISO 20022 adoption is progressing across major payment markets. In the United States, CHIPS migrated in April 2024, Fedwire followed in July 2025, and FedNow, launched in 2023, was built on ISO 20022 from inception. In the United Kingdom, CHAPS and the RTGS system have transitioned, with enhanced data requirements planned for later phases. Across Europe, platforms such as T2 and SEPA already operate on ISO 20022 standards.

While compliance deadlines drive adoption, the true value of ISO 20022 lies in how banks use the data operationally. Without changes to workflows, systems, and operating models, many of the benefits remain unrealized.

Structured data alone does not resolve the inefficiencies caused by fragmented investigation workflows. To realize the full value of ISO 20022, banks need orchestration capabilities that coordinate how investigations are initiated, routed, managed, and resolved.

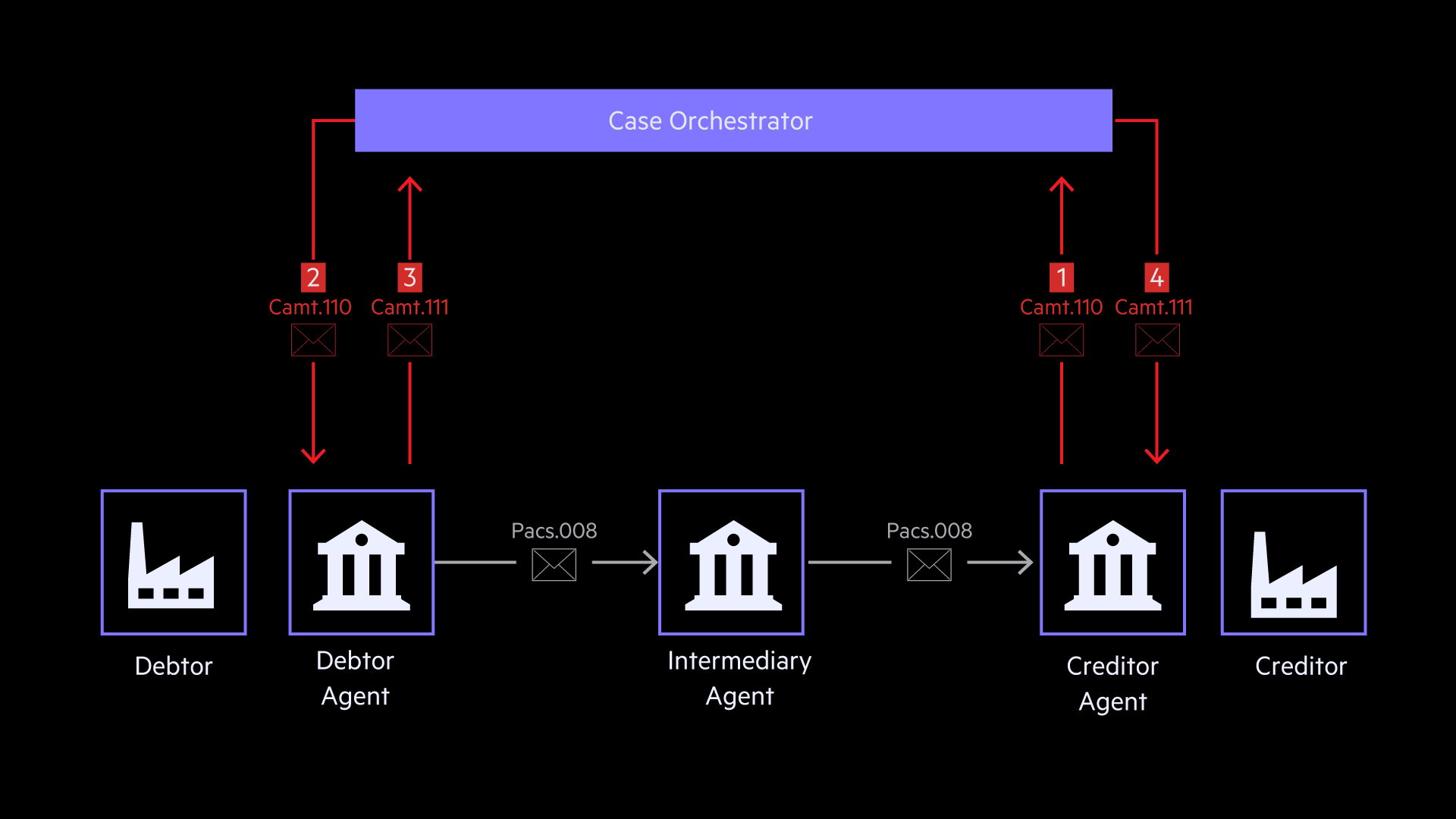

SWIFT Case Orchestrator provides a centralized framework for managing investigations across institutions. Instead of relying on serial message chains, cases are initiated and tracked through standardized ISO 20022 messages. As shown in the following figure, when a creditor raises an inquiry using a camt.110 message, the orchestrator routes the case directly to the institution best positioned to respond. Responses are returned through camt.111 messages, creating a clear and auditable case lifecycle.

Centralized dashboards provide real-time visibility into case status, response times, and SLA performance. This transparency reduces follow-ups, improves accountability, and allows operations teams to manage workloads more effectively.

Modern investigation platforms typically share several architectural characteristics. A unified case layer consolidates investigation data across payment rails and channels. Intelligent routing prioritizes cases based on urgency, client impact, or regulatory requirements. Structured ingestion capabilities normalize data from ISO 20022 messages, legacy formats, APIs, and even unstructured sources. Embedded compliance controls ensure auditability, access management, and regulatory alignment. Analytics and reporting tools convert operational data into insights that support continuous improvement.

For mid-sized banks, this architecture supports incremental modernization without the complexity or cost of large enterprise systems.

Many banks operate with a mix of tools that have evolved over time. In-house solutions such as spreadsheets and email trackers remain common due to their flexibility and low cost, but they are fragile and difficult to scale. Enterprise-grade investigation platforms offer advanced automation and analytics, but their cost and implementation complexity can be prohibitive for mid-tier institutions.

SWIFT utilities support routine investigation use cases but often lack broader orchestration, analytics, and integration capabilities. As a result, mid-sized banks frequently find themselves caught between manual processes and enterprise platforms that exceed their needs and budgets.

This gap becomes more pronounced as payment volumes grow and ISO 20022 adoption accelerates. Siloed case queues, limited visibility, and partial data integration make it difficult to meet customer expectations or regulatory scrutiny. There is a clear need for modular, flexible solutions that can evolve alongside the bank’s payments strategy.

.webp)

Seizing the Opportunityto Enhance Customer Experience

ISO 20022 migration should be treated as a strategic modernization initiative rather than a narrow compliance project. A phased approach helps banks manage risk, control costs, and deliver measurable improvements at each stage.

The first phase focuses on assessment and prioritization. Banks map existing investigation workflows, identify bottlenecks, and prioritize high-volume or high-risk payment corridors. Alignment between operations, IT, and compliance teams is essential to define objectives and success metrics.

The second phase addresses data ingestion and parsing. Systems are upgraded to fully parse ISO 20022 messages while maintaining compatibility with legacy MT formats during the transition period. Data quality and validation rules are critical at this stage.

The third phase introduces orchestration and visibility. Automated routing, escalation rules, and SLA tracking are implemented to reduce manual intervention and improve transparency. Dashboards provide real-time insight into workloads and performance.

The final phase embeds the new model operationally. Investigation workflows are scaled across domestic, cross-border, and instant payments. Staff are trained, escalation procedures refined, and compliance controls embedded into daily operations. Continuous improvement processes ensure the framework remains aligned with evolving standards and regulatory expectations.

Common challenges include over-customization, insufficient testing, and underestimating the importance of change management. Addressing these early improves long-term outcomes.

ISO 20022 marks a turning point for payment investigations. By combining structured, data-rich messages with orchestration platforms such as SWIFT Case Orchestrator, banks can significantly reduce resolution times, lower operational costs, and improve transparency for customers and internal teams.

Modernizing investigations is no longer optional. Institutions that move early gain stronger operational resilience, improved compliance posture, and better customer experience. ISO 20022 is not simply a messaging upgrade. It provides the foundation for a more efficient, scalable, and future-ready payments landscape.

Note : As per Swift’s Knowledge Centre note with ID 5026406 and date 16 March 2026, the Stop & Recall requirements for SR2026 have been updated. Stop & Recall is no longer mandatory for all financial institutions. However, the SWIFT SR2026 requirements for Exceptions and Investigations remain in place, and banks are still required to receive camt.110 investigation requests with an embedded MT 199 through Case Management.

.png)

.png)