.png)

.png)

When banking services go offline or slow down, customers experience failed payments, delayed transfers, login issues, interrupted card use, and poor service. Internally, outages create pressure on operations teams, increase manual workloads, delay issue resolution, and expose banks to financial and regulatory consequences.

While these incidents appear to be isolated technology failures, the root causes often stem from challenges with legacy systems, including disconnected processes, limited scalability, and low automation. Pega helps banks address these root causes through intelligent workflow automation, system orchestration, scalable architecture, and phased modernization strategies that reduce disruption and improve resilience.

A legacy system comprises hardware, software, databases, and business processes built on outdated technologies or architectures. These systems are often developed using older programming languages and run on obsolete or unsupported hardware and software platforms.

As a result, legacy systems carry a high risk of accumulating technical debt and operational inefficiencies, making them difficult to maintain, scale, and integrate with modern solutions.

Legacy system transformation is essential because it improves scalability, reduces downtime, enhances security, and enables organizations to stay competitive.

Addressing legacy system challenges is critical for banks to reduce downtime, enhance security, and remain competitive. Institutions that continue to rely on outdated systems are more prone to outages due to architectural complexity, integration gaps, and infrastructure limitations.

Legacy systems were often designed to prioritize stability, consistency, and reliability for known workloads, especially in banking. But in today’s world, stability means a system that is 24/7 available, maintains real-time transaction history, and scales up when customer demand spikes. As banking operations grow, systems must scale accordingly.

Built on monolithic architectures, the application components, such as the user interface, business logic, and data access, are tightly coupled. It operates as a single, unified service, making it ideal for simple, small-scale applications or for rapid development. Such systems are difficult to scale, and a failure in one component can bring down the entire system.

Disconnected Integrations Create Cross-system Operational Failures

Legacy systems often run on outdated technologies that are difficult to integrate with modern cloud-based platforms. Over time, banks add digital channels, CRM platforms, payment gateways, reporting systems, and third-party services. Differences in data formats, communication protocols, or APIs make it challenging to connect old and new systems.

Disconnected integrations make it difficult to achieve real-time data visibility across platforms. For instance, a slowdown in identity verification can impact onboarding, payments review, account servicing, and customer notifications simultaneously. In many cases, the issue is not the newly added tools or platforms, but the lack of orchestration and integration.

Increasing Transaction Volumes Expose Infrastructure Limits

Legacy systems were often designed to process data in batches rather than in real time. They struggle with increasing real-time transaction volumes required for modern mobile and digital commerce.

When millions of users simultaneously attempt UPI payments and legacy systems reach their fixed capacity limits, they begin failing. This has led to frequent technical failures at checkout, where the user's money is deducted but the merchant doesn't receive it, resulting in a poor customer experience and regulatory scrutiny.

Longer Processing Cycles

Legacy systems often require manual input or data transfers, which slow operations and introduce human error. Repetitive tasks that modern AI-driven systems can complete in seconds can take hours or days, creating significant bottlenecks.

Legacy banking environments often store payment data across separate core systems, middleware layers, and outdated operations tools that do not communicate seamlessly. In payment investigation teams, this creates heavy dependence on manual work when a customer reports a delayed or missing international transfer. As a result, a case that modern orchestrated platforms resolve in minutes may take hours or days in a legacy environment.

Expanded Cybersecurity Vulnerabilities

Many legacy systems still rely on single-factor password authentication and have limited role-based access controls. This allows every user to access all the information the system holds.

Additionally, the system runs outdated software that no longer receives security patches. This creates exploitable security vulnerabilities.

Slow Response to Changing Regulatory Requirements

Banks operate under constant pressure to implement new mandates, reporting requirements, data retention rules, payment standards, and consumer protection controls.

When policy changes must be hardcoded across multiple systems, each update introduces testing overhead, deployment risk, and potential downtime. This is especially visible in institutions where business rules are embedded deep within legacy applications rather than managed centrally. The faster regulations change, the more fragile the outdated architecture becomes.

Downtime is a serious business risk because it disrupts critical operations. Even a short disruption frustrates customers and interrupts internal operations. The major consequences of bank downtime include:

The rip-and-replace concept, which involves replacing legacy technology in its entirety, often fails or underperforms because it is expensive, risky, and disruptive. Such programs may appear successful at first, but even a single defect can significantly disrupt operations.

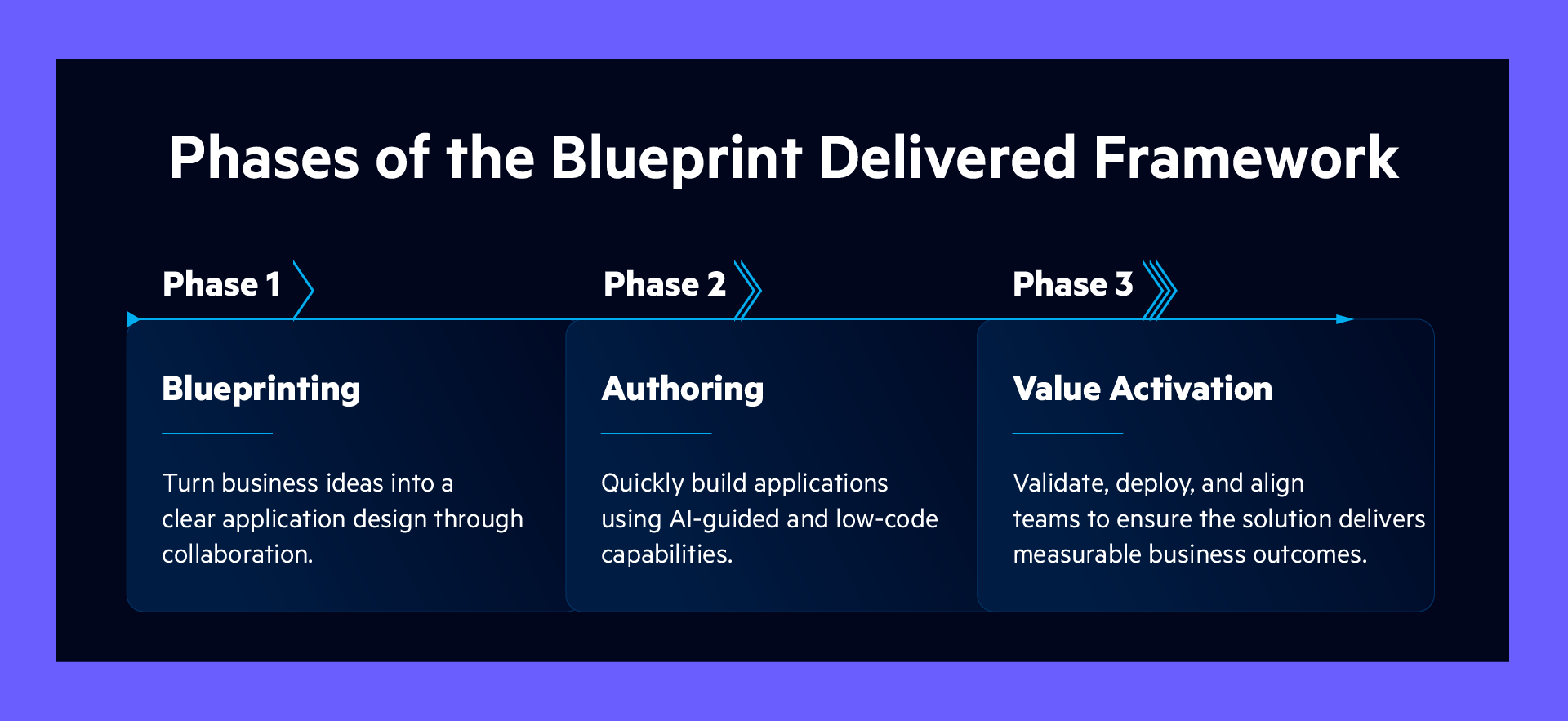

Pega helps with legacy transformation through AI-powered discovery, low-code application development, and phased modernization strategies to replace outdated systems. It reduces downtime by allowing new applications to run alongside legacy systems during transition, enabling a "gradual shift" called Pega Express Phases rather than a risky "rip-and-replace" approach. Today, Pega uses the Blueprint Delivered framework to accelerate the delivery of transformations.

Blueprint Delivered framework uses Pega GenAI as the new standard for application discovery and design. These phases work together as a continuous flow, helping organizations move seamlessly from idea to implementation. The framework includes three phases:

Phase 1: Blueprinting

The Blueprinting phase focuses on transforming business ideas into a well-defined application design. It brings together discovery and design through real-time collaboration, ensuring both business and technical stakeholders are aligned early in the process.

Phase 2: Authoring

Once the blueprint is ready, the Authoring phase shifts focus to building the application efficiently. Using AI-guided and low-code capabilities, teams can quickly convert the blueprint into a working solution.

Phase 3: Value Activation

The final phase, Value Activation, ensures that the application is ready for real-world use and delivers measurable outcomes. It involves validating the solution, finalizing deployment, and aligning stakeholders before go-live.

Pega helps banks address other legacy system challenges by providing a unified platform that connects systems, automates workflows, scales operations, and strengthens operational control.

Orchestrates Work Across Disconnected Systems

Pega Agentic Process Fabric serves as the orchestration layer, seamlessly connecting systems, customers, and employees. Instead of managing work in disconnected applications, banks gain end-to-end visibility, intelligent handoffs, and coordinated execution across the enterprise.

Scales Operations as Demand Increases

Pega is designed to support enterprise-scale workloads with flexible deployment options and an architecture that can grow with demand. Banks can handle rising volumes, expanding processes, and new digital journeys without repeatedly redesigning operating models.

Intelligent Automation Solution

Pega for banking automation helps to move beyond isolated task automation by combining workflow automation, AI-driven decisioning, robotic automation, and case management on a single platform. This allows organizations to automate end-to-end processes across teams and systems, accelerate turnaround times, improve consistency, and free employees to focus on higher-value customer and risk activities.

In banking environments where the risks of downtime, regulatory pressure, and legacy complexity arise, institutions need a partner that can modernize critical systems without disrupting everyday operations. EvonSys combines deep Pega expertise with proven delivery experience across enterprise-scale transformation programs.

A global financial institution needed to upgrade a highly complex Pega environment that supported millions of daily transactions, where even minor disruptions could affect critical banking operations.

EvonSys led the transformation through a structured upgrade program, using a backward-compatible approach that allowed legacy and upgraded applications to run in parallel on a unified database.

This enabled a controlled transition with near-zero downtime while improving platform stability and reducing upgrade risk.

Connect with EvonSys to automate banking operations using Pega and build a future-ready enterprise.

.png)

.png)