Evonsys is propelling industries into the future, transforming operations and customer experiences with low-code solutions that unlock unprecedented levels of efficiency and innovation.

Since 2015, Evonsys has harnessed the power of low code to refine global organizations. We've revolutionized sectors from banking to retail with our comprehensive solutions, focusing on risk mitigation, management optimization, and streamlined automation for unrivaled efficiency.

Why Payment Investigation Delays Have Become a Critical Operational Risk for Banks

Why Payment Investigation Delays Have Become a Critical Operational Risk for Banks

Chandana Chalamalasetti

April 22, 2026

HIGHLIGHTS

Discover why payment investigations are falling behind modern payment ecosystems, creating operational risk and costing banks over USD 1.6 billion annually.

Understand the hidden costs of delays, including operational inefficiency, liquidity strain, compliance pressures, and reputational impact.

Explore how automation, centralized case management, and enhanced payment visibility can transform investigation bottlenecks into a strategic advantage.

The payments landscape has changed significantly over the last few years. They are faster, more transparent, and increasingly real-time. In many corridors, funds reach the beneficiary bank within minutes or hours. But when something goes wrong, teams still need days to figure out what happened across a bank payment investigation.

That gap is not a small operational issue anymore. It is becoming a structural weakness. Industry data shows that while most cross-border payments are processed quickly, investigations still take five to ten working days to resolve. And the cost of that gap is not marginal. Banks collectively spend over USD 1.6 billion annually investigating delayed payments.

This is where the shift is happening. Payment investigation delays are no longer just inefficiencies; they are emerging as a measurable operational risk.

What Slows Down Payment Investigations

Payment Investigations: The Most Overlooked Part of Payments

If you look at your payments stack, most of the focus has gone into speed, straight-through processing, and customer experience. Investigations, on the other hand, have remained largely unchanged.

When a case is raised, your teams still:

Pull data from multiple systems

Check message formats and transaction references

Reach out to counterparties

Wait for responses

Even today, investigations often involve multiple back-and-forth emails and manual follow-ups across banks, which makes the process slow and resource intensive. And this is happening in a world where everything else in payments is becoming real time.

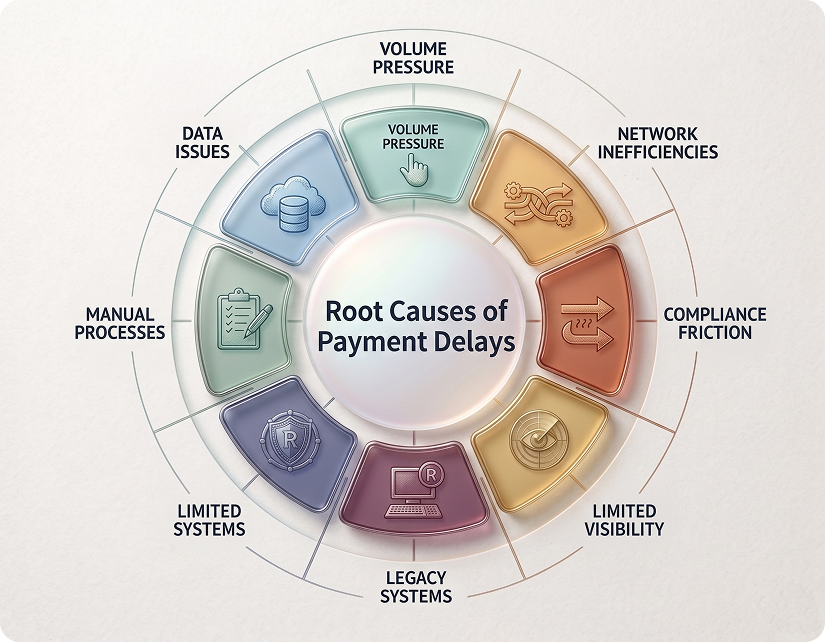

Payment investigation delays are rarely caused by a single issue. They usually stem from a combination of process, data, technology, and ecosystem constraints across banks, payment schemes, and correspondent networks. Below is a clear, industry‑aligned breakdown of the root causes:

Incomplete Payment Data

One of the most persistent causes of payment investigation delays is inadequate data quality. Many cross‑border payments still rely on legacy messaging formats where critical details such as remittance information, party identifiers, or references like the UETR are missing, inconsistent, or embedded in free text.

Even with the migration to ISO 20022, coexistence with MT messages and imperfect data translation often result in loss of structure. As a result, investigators must manually reconstruct payment details, seek clarification from counterparties, or raise additional queries, significantly extending resolution timelines.

Fragmented and Manual Investigation Processes

Payment investigations are often handled across multiple systems and teams, with no unified view of a case. Operations, payments, compliance, and customer service typically work in silos and rely on emails, spreadsheets, or manual trackers to coordinate investigations.

A high dependence on human intervention for case initiation, tracking, and follow‑ups slows processing and increases the likelihood of errors. Without standardized workflows or automation, even straightforward exceptions take longer to resolve.

Inefficiencies in the Correspondent Banking Model

Cross‑border payments frequently pass through multiple correspondent banks, each introducing potential delays. Visibility beyond the first or second intermediary is limited, making it difficult to identify where a payment is held or processed slowly.

Response times vary across correspondents, and binding service‑level agreements for investigations are often absent. Non‑standard communication practices and repeated clarification cycles further extend investigation timelines, particularly when multiple intermediaries are involved.

Limited Case Orchestration and Exception Management

Many banks continue to approach payment investigations in a reactive manner, initiating cases only after customer complaints or internal escalations. There is limited capability to proactively detect stalled or at‑risk payments early in the lifecycle.

In addition, the lack of intelligent case orchestration means investigations are not prioritized based on value, urgency, customer importance, or regulatory risk. As a result, high‑priority cases are frequently delayed alongside low‑value exceptions.

Compliance and Regulatory Friction

Sanctions screening and AML controls are significant contributors to investigation delays. Incomplete or ambiguous party data often leads to false positives, causing payments to be placed on hold while manual reviews are performed.

Case ownership is not always clearly defined, particularly when compliance and operations teams work in separate systems. Investigations may also stall due to missing regulatory documentation such as invoices or purpose‑of‑payment details that must be obtained from customers or counterparties.

Lack of End‑to‑End Payment Visibility

Limited transparency across the payment lifecycle forces banks to spend considerable time tracing payment status. Updates are not consistently shared across the correspondent chain, and confirmations may be delayed or incomplete. Although tracking tools such as SWIFT GPI are available, inconsistent adoption and manual interpretation reduce their effectiveness. This lack of clear visibility increases inquiry volumes and lengthens resolution cycles.

Legacy Technology Constraints

Many payment platforms were designed without modern investigation requirements in mind. Rigid systems lack flexible workflows, seamless integration with case management tools, and full support for structured ISO 20022 data.

Weak data lineage and audit trails make it difficult to determine what happened to a payment, when it occurred, and why. Investigators therefore spend time reconstructing events instead of resolving the issue itself.

Volume Pressure and Operational Strain

Rising transaction volumes, driven by real‑time payments and growing cross‑border flows, have increased both the frequency and complexity of payment exceptions. At the same time, investigation teams often face resource constraints and skills gaps, particularly in understanding ISO 20022 data structures. Dependence on a limited number of experienced specialists creates bottlenecks, while operational backlogs grow quickly during peak periods.

What Delayed Investigations Really Cost Banks

The Hidden Costs of Payment Investigation Delays

Payment investigation delays are often treated as routine back-office issues, but their impact goes beyond missed service levels and customer dissatisfaction. Each delay creates a ripple effect across revenue, risk, compliance, and trust. For banks operating at scale, these hidden costs are becoming increasingly difficult to sustain.

Operational Inefficiency

Payment investigation delays create a sustained operational burden. Manual case handling, repeated follow-ups, and fragmented workflows increase the effort required for each investigation while limiting throughput and impacting overall banking operations efficiency. As volumes grow, these inefficiencies scale with them. What seems manageable at lower volumes becomes a capacity constraint as transaction volumes rise, data formats expand, and exception scenarios become more complex.

Impact on Customer Trust

Long investigation timelines reduce confidence in the bank’s ability to manage payments reliably. Corporate and institutional clients depend on timely settlement, clear visibility, and predictable resolution cycles to manage liquidity and meet obligations. When investigations lack transparency or defined timelines, customers raise repeated queries, escalate issues, and file complaints. Over time, this weakens trust and puts client relationships at risk.

Financial and Liquidity Exposure

Delays in investigations have direct financial impact. Unresolved payments, especially high-value and cross-border transactions, lock liquidity, disrupt intraday funding, and affect cash flow planning. Missed service commitments can lead to compensation, interest adjustments, and penalties. Indirect costs also increase as skilled teams spend more time on exception handling instead of strategic work.

Heightened Risk and Compliance Pressure

Long investigation cycles reduce visibility into root causes such as sanctions issues, fraud signals, data gaps, or processing errors. As cases remain open, operational uncertainty increases along with regulatory and reputational risk. With stronger regulatory focus on timeliness and traceability, slow and manual processes increase the likelihood of audit findings and control gaps.

Strategic and Reputational Impact

Persistent delays affect how the bank is perceived in the market. Institutions that resolve payment issues slowly are seen as less reliable by correspondent banks, fintech partners, and corporate clients. In a payments environment driven by speed and transparency, these delays limit the bank’s ability to compete, build partnerships, and scale innovation.

There is a clear shift happening across the industry. Banks are beginning to recognize that payment investigations cannot remain a reactive process.

Instead, they need to be:

Structured

Integrated across systems

Supported by investigation automation

Built for scale

Solutions that centralize case management, leverage ISO 20022 data, and provide real-time tracking are driving tangible improvements. Streamlined payment investigation processes can accelerate resolution and reduce operational costs, turning a persistent bottleneck into a strategic advantage.

Conclusion

Conclusion

The disconnect between instant payment clearing and multi-day investigations has transformed a process of inefficiency into a critical operational risk. Banks can no longer sustain the high costs of manual workflows or the reputational damage caused by slow resolution cycles.

To thrive in a real-time environment, the industry must shift from reactive troubleshooting to automated orchestration. By leveraging ISO 20022 data, eliminating internal silos, and adopting centralized case management, banks can streamline investigations, minimize delays, and enable faster payment resolution.

See how leading banks are restructuring payment operations to reduce investigation delays

.png)

.png)

.png)

.webp)

.png)

.png)