.png)

.png)

Banks are under constant pressure to modernize their operations, launch new services faster, and deliver a seamless customer experience.

To modernize their operations, banks face many challenges, including selecting the right platform, staying within budget and meeting timelines, implementing effective strategies, and integrating modern applications with existing systems.

Customer expectations have also evolved significantly with the rise of digital banking. Today’s customers expect faster responses, transparent processes, and consistent service across digital channels. However, many banks still rely on fragmented legacy systems and manual processes, making it difficult to deliver these experiences while maintaining strict compliance and data security standards.

To address these challenges, many financial institutions have started implementing low code solutions, as they fit with their expectations. However, not all low-code platforms are designed to support the complexity of banking environments.

The platform Pega built for banking environments helps resolve these challenges by orchestrating customer journeys, enabling intelligent automation, and managing complex cases within a single workflow ecosystem. For banks evaluating low-code platforms, the real question is whether the platform can support the scale, governance, and operational intelligence required in modern banking. In this blog, we explore why many banks choose low-code solutions to modernize processes while maintaining compliance and operational efficiency.

Banking operations rely on systems that process large volumes of transactions while keeping data reliable across different systems. Every process, from customer onboarding to dispute resolution, requires strict compliance with financial regulations, accurate data handling, and coordination across multiple internal and external systems. They face multiple challenges, including:

Legacy systems are often built as standalone units, making it difficult to connect with next-generation platforms. It's strongly advised to transform legacy systems, even though many banks still rely on them. Information is frequently stored in separate systems, which makes it hard to get a single, real-time view of customer activity.

Since banking operations handle millions of transactions, moving data across legacy systems during patching or integration can lead to data loss or inconsistencies. Developers face challenges when integrating legacy systems with modern, user-friendly front-end applications, enabling modernization without complete overhauls.

Processes such as payment investigations, dispute handling, and loan servicing require multiple steps, stakeholder collaboration, and continuous tracking of case progress.

The payment investigations are complex because they require the banking team to manually trace transactions across different payment rails, such as SWIFT, analyze message flows, and coordinate with the corresponding banks and payment processors. It doesn’t end here, as they need to comply with strict regulatory and SLA-driven resolution timelines. When information is spread across disconnected systems, investigation teams often need to access multiple platforms to collect transaction details and supporting evidence. This manual effort increases operational inefficiencies and introduces human error.

Dispute handling in banking is operationally complex because it requires banks to manage chargebacks across multiple card networks, validate transaction evidence, coordinate with merchants and payment processors, and comply with strict regulatory and network-specific dispute timelines.

Banks must adhere to evolving global and regional regulations such as KYC, AML, and data protection laws, ensuring that every workflow is auditable and governed.

Without intelligent workflow orchestration, these processes can become slow and error-prone.

Banks must maintain detailed audit trails, enforce regulatory rules, and ensure operational transparency across every workflow. Legacy banking platforms are typically built on monolithic architectures, where business logic, transaction processing, and compliance rules are tightly coupled within the same application stack. They are never designed to meet modern data privacy standards.

When regulations change, banks must:

This makes regulatory updates slow, risky, and expensive.

To address these challenges, banks increasingly require intelligent low code platforms that support end-to-end case management, automation, and governance.

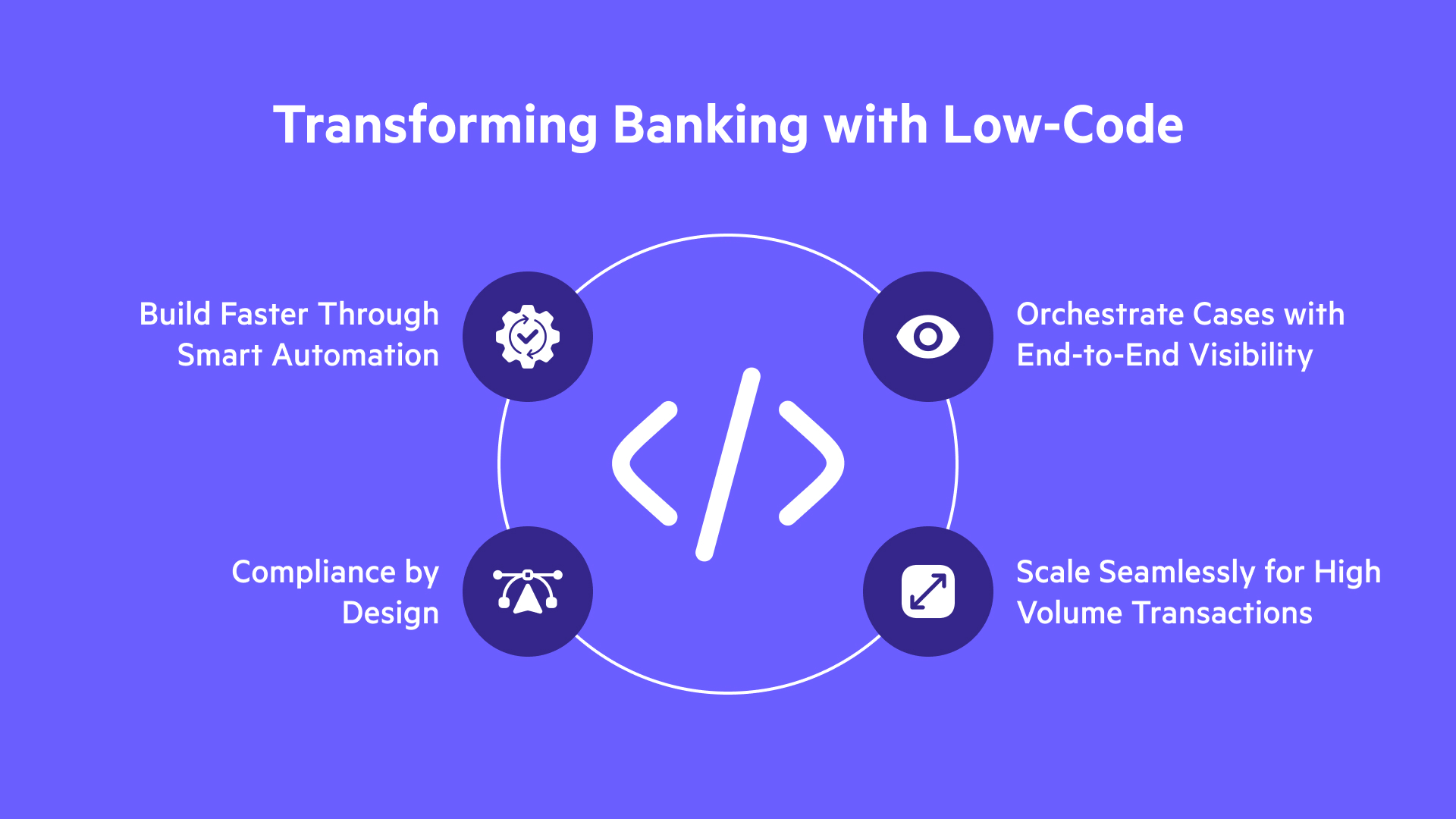

Below are four key capabilities that make low-code platforms particularly effective in banking environments.

Low-code platforms allow development teams to create applications through visual modeling, reusable components, and drag-and-drop tools. Instead of writing large amounts of code, developers and business teams can work together to design workflows and interfaces directly within the platform.

For banks, this significantly reduces the time required to launch new operational tools. Faster development cycles allow them to respond quickly to evolving customer expectations and competitive pressures.

Low code for banking operations provides built-in workflow orchestration and case management capabilities, enabling banks to model and automate these processes. Each transaction or request can be managed as a case that moves through defined stages with automated routing and real-time visibility.

Regulatory compliance is a fundamental requirement in banking. Applications must ensure consistent rule enforcement, secure data access, and complete operational transparency.

Low-code platforms incorporate governance frameworks, rule-based decision management, role-based access controls, and audit trails directly into the development environment. This ensures that banking applications remain compliant with regulatory standards while enabling operational processes to evolve.

Banks process millions of transactions daily across payments, transfers, and digital banking services. Operational platforms must therefore support high concurrency while maintaining performance and data integrity.

Low code platforms, especially Pega, help in banking architecture to support scalable processing through distributed workflows and optimized transaction handling.

While low code for banking offers significant advantages for modernizing financial operations, banks must carefully evaluate whether a platform can support the complexity of their operational environment. Factors such as scalability, case management capabilities, governance, and integration flexibility are critical when selecting the right platform for banking workflows.

Understanding these requirements helps banks move beyond generic low-code solutions and identify platforms specifically designed to support enterprise-scale banking operations.

Choosing the right implementation partner becomes critical during modernization. EvonSys helps financial institutions design, implement, and scale low-code solutions that align with operational requirements. With deep experience in banking workflows and enterprise automation, EvonSys supports banks in accelerating digital transformation while ensuring governance, compliance, and long-term scalability

Explore our next blog to learn how Pega outperforms other low code platforms in banking environments.

.png)

.png)