.png)

.png)

It starts with a call no issuer wants to see in their queue.

A cardholder spots an unfamiliar transaction on their statement or has issues with the merchandise or the merchant. The transaction is already settled. The merchant details are vague. The cardholders call the contact center, frustrated, and confused. A dispute is raised, documentation is requested, timelines kick in, and what could have been a simple off the Network resolution now begins its journey towards chargeback adjudication.

By the time the dispute reaches the issuer’s back office for investigation, the incident has already happened, funds are in motion, costs accumulating and customer trust is at stake.

For most banks and financial institutions, this scenario is routine rather than exceptional with huge financial implications. It highlights a deeper issue in how disputes are approached, as they are often treated as isolated inevitable events instead of outcomes shaped earlier in the transaction lifecycle. When disputes are viewed through this lens, the opportunity becomes clear. By intervening upstream and addressing root causes early, issuers can shift from reactive resolution to proactive prevention, reducing disputes before transactions escalate into incidents.

This blog outlines the practical measures issuers can take at every stage of the transaction lifecycle to avoid disputes and chargebacks.

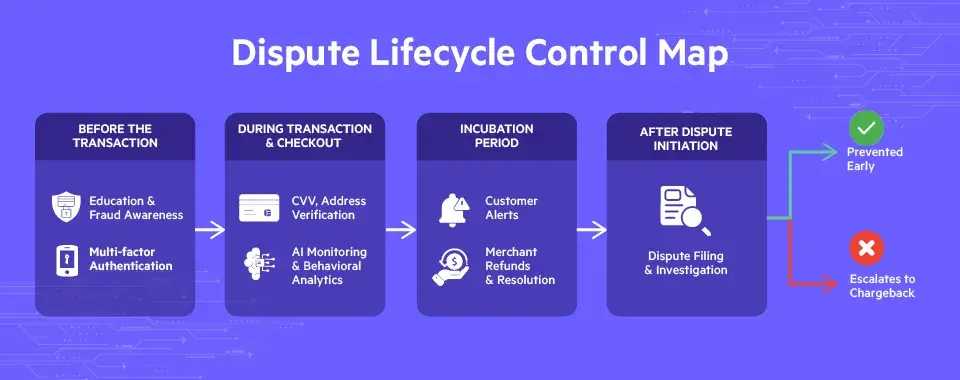

Effective dispute management starts well before a transaction is initiated and extends beyond authorization into the post-transaction incubation period where transactions become a potential ticking time bomb. Modern issuer strategies are designed to intercept risks early, applying intelligence and controls to reduce disputes before they escalate into chargebacks.

Disputes often stem from simple lapses like shared credentials, weak passwords or PINs, unsecured devices, or unrecognized merchant activity. Issuers can reduce this risk by:

As fraud tactics evolve, issuers must invest in:

Proactive audits of systems, processes, and people, including access controls, operational procedures, and adherence to fraud policies, help uncover vulnerabilities before they are exploited. These assessments ensure fraud prevention strategies remain effective as transaction volumes, channels, and organizational roles evolve.

Robust cybersecurity protocols and smart authentication methods, such as multi-factor verification and controlled access to sensitive systems, protect sensitive data and reduce exposure to unauthorized activity, one of the most common precursors to disputes.

At this stage, issuers have the highest opportunity to stop fraud and disputes before funds are committed, while still preserving a seamless customer experience.

Prevention begins with ensuring that transactions are both intentionally approved and initiated by the right party. Cardholders must be educated to review transactions carefully before approval, while issuers reinforce this step with strong authentication mechanisms. Multi-factor authentication across channels helps verify identity and reduce unauthorized activity, especially for digital and card-not-present transactions.

Cardholders should approve charges with full visibility into pricing, refund terms, and cancellation policies. In cases involving unfamiliar or high-risk merchants, issuers review adds a critical second layer of protection by validating transaction legitimacy before settlement. When necessary, issuers can confirm intent with the customer or block transactions before settlement.

Several validation checks help identify suspicious activity in real time:

These controls add friction only where risk exists, while significantly reducing downstream disputes.

Analyzing transaction frequency, quantity, and historical behavior helps surface abnormal patterns that may indicate fraud. Geo-location verification further strengthens detection by comparing IP data with billing and shipping addresses, enabling issuers to identify inconsistencies before transactions are completed.

Transactions should be screened against merchant activity databases, whether maintained internally or through third-party sources, to block known high-risk merchants. In some cases, issuers may also delay posting transactions until merchandise is shipped or delivered, aligning settlement timing with fulfillment and reducing disputes related to non-receipt.

Tokenization replaces sensitive card data with one-time credentials, ensuring merchants never access actual card information. This lowers the risk of data compromise and future fraud. In parallel, securing online banking passwords and PINs remains essential to protecting account access during the transaction process.

Not all disputes surface immediately. The period after a transaction is approved but before a customer raises a complaint is a critical window where early signals can still prevent escalation.

Review approved transactions for patterns across merchants, geographies, and customer behavior to identify emerging risk before disputes occur.

Use AI and ML to detect unusual transaction patterns, screen actors against trusted risk databases, and help issuers intervene before transactions result in disputes.

Manually assess complex or layered transactions that may bypass automated rules and indicate sophisticated fraud.

Provide real-time alerts and clear transaction details to help customers quickly recognize and report unauthorized activity without initiating a dispute.

Provide clear transaction descriptors and statements to reduce confusion around unrecognized or misidentified purchases.

Detect abnormal patterns and trigger compliance or operational reviews before a dispute is formally raised.

Exchange insights with partner institutions to identify common fraud trends and strengthen preventive controls.

Even with strong preventive controls, disputes are unavoidable. At this stage, the objective shifts from prevention to containment, ensuring disputes are resolved quickly and do not escalate into chargebacks.

Guide the customer to resolve disputes by contacting merchants early to validate transactions and clarify order details before formal chargeback timelines begin.

Reduce confusion by providing detailed order insights and enriched transaction information through third-party networks, helping cardholders recognize legitimate purchases.

Make merchant refunds visible to the customer and issuer via third-party resolution frameworks if needed, stopping disputes before they progress into full chargebacks.

Where appropriate, issuers can proactively refund transactions through write-offs to close disputes quickly and prevent further escalation.

Use card network programs that notify merchants of impending disputes and provide a limited window to resolve them through refunds before chargebacks are raised.

Apply rules-based decision engines to automatically resolve eligible disputes, helping maintain healthy dispute-to-transaction ratios while reducing operational effort.

While payment issues and fraud-related disputes are inevitable, not all of them should end in chargebacks. A strong fraud and dispute management system such as Pega Smart Disputes, acts as a gatekeeper, helping issuers identify where preventive strategies are leaking and ensuring that truly unavoidable disputes move forward to chargeback.

By combining preventive controls with a smart dispute solution, financial institutions can significantly reduce chargeback-related losses while gaining valuable intelligence into dispute patterns, root causes, and process gaps. Over time, these insights help fine-tune enterprise dispute management strategies, shifting the focus from reactive handling to proactive prevention.

EvonSys helps financial institutions go beyond reactive dispute handling by designing and implementing intelligent, prevention-first dispute strategies using Pega. Our experience across complex dispute and investigation transformations enables banks to not only streamline chargeback operations, but also continuously fine-tune their enterprise dispute management processes with data-driven insights.

As the payments and dispute landscape continues to evolve, the most effective strategies will be those that combine strong preventive controls with smart, insight-driven execution. This shift requires not just the right technology, but the right approach, one that treats dispute management as a strategic capability, not a last-resort process.

Stop Chargebacks Before They Start

Intervene earlier in the transaction lifecycle to minimize dispute-related losses.

.png)

.png)