Evonsys is propelling industries into the future, transforming operations and customer experiences with low-code solutions that unlock unprecedented levels of efficiency and innovation.

Since 2015, Evonsys has harnessed the power of low code to refine global organizations. We've revolutionized sectors from banking to retail with our comprehensive solutions, focusing on risk mitigation, management optimization, and streamlined automation for unrivaled efficiency.

From Bilateral Messaging to Shared State: How Swift’s Transaction Manager Redefines Payment Architecture

From Bilateral Messaging to Shared State: How Swift’s Transaction Manager Redefines Payment Architecture

January 21, 2026

HIGHLIGHTS

ON THIS PAGE

This article outlies how with the occasion of the ISO 20022 migration the Swift network has introduced a central transaction data integrity capability that results in a consistent, deterministic processing logic. It is crucial for Financial Institutions' payments and sanctions back-office teams to understand these capabilities and also to ensure they maintain end-to-end visibility and investigation efficiency through interconnected use cases including domestic and other non-SWIFT Swift networks.

For more than four decades, cross-border payments have relied on a bilateral messaging model. It worked for a long time, but it also created fragmentation and led to the same recurring problems: isolated views, inconsistent records, missing data, and hours of reconciliation work. As payment volumes grew and regulatory expectations increased, the cracks in this model became harder to ignore.

When the Swift network was first introduced, its purpose was clear: enable secure, standardized end-to-end messaging between financial institutions. Each bank exchanged messages with the next party in the chain, performed its own checks, and maintained its own internal view of the transaction.

As cross-border payments evolved, additional layers were added to this model. Swift gpi made it possible to assemble an end-to-end transaction view by linking individual messages together, improving transparency and traceability. The subsequent migration to ISO 20022 introduced richer, more structured data, raising expectations for interoperability, automation, and data quality.

As ISO 20022 adoption accelerated, it became evident that a format change alone was not sufficient. Supporting coexistence between new MX messages and legacy MT messages, while preserving data consistency across institutions, required a new coordination layer. The introduction of Swift Transaction Manager (TM) addressed this need.

Transaction Manager does not replace messaging. Instead, it builds on these earlier evolutions by introducing a shared transaction copy together with stricter validation and central data integrity rules, reshaping how cross-border payments are coordinated on the Swift network.

Why Bilateral Messaging is No Longer Enough

The bilateral messaging model was designed for a payment landscape with lower data volumes and simpler processing requirements. In today’s environment, several limitations have become increasingly apparent.

Fragmented transaction views

Each bank maintains its own version of the payment, which can diverge as updates and repairs are applied independently. Reconciling these differences requires manual effort and becomes especially challenging during investigations.

Legacy constraints with richer data

ISO 20022 introduces detailed, structured fields with defined semantics. Legacy MT messages cannot reliably carry this richness, leading to data truncation, free-text workarounds, and inconsistencies that affect downstream processing.

Investigations remain reconstruction exercises

Even with gpi tracking, investigations often require piecing together information from other networks, multiple messages and internal records. The absence of a single authoritative transaction view slows resolution and increases operational workload.

Inconsistent outcomes across institutions

Because each bank processes its own copy of the data, validation outcomes and downstream handling can vary, increasing operational risk and reducing predictability across the chain.

The Core Concept Behind Transaction Manager: Shared Transaction State

The most important idea behind Transaction Manager is the shift from just passing messages from one institution to the next, to maintaining a single, shared view of each payment transaction. Instead of every bank holding its own version of the transaction, Transaction Manager keeps one central representation that everyone can refer to.

When an in-scope payment enters TM, a transaction copy is created using ISO 20022 structures. This transaction copy serves as a common reference point for participating institutions, reducing data drift and ensuring alignment across the payment lifecycle.

Rather than treating a payment as a loose sequence of messages, TM enables it to be managed as a single transaction progressing through defined lifecycle states.

This model rests on three foundational principles.

One Canonical Transaction Copy

The transaction copy represents the authoritative version of the payment on the Swift network. All participants read from and contribute to this shared record, subject to defined visibility rules. This eliminates conflicting interpretations and missing data that commonly arise in bilateral flows.

State-Driven Lifecycle Progression

The Transaction Manager coordinates payments through explicit lifecycle states. Actions such as instructing, confirming, transferring, crediting, or rejecting a payment update the transaction state rather than creating independent message chains. TM orchestrates these updates and notifies relevant participants, keeping all parties synchronized.

Network-Level Validation and Data Integrity

Transaction Manager applies stricter validation and data integrity rules. Data elements are classified as editable or locked, defining which fields may be updated during processing, and which must remain unchanged.

Based on these rules, the Transaction Manager will either update the transaction copy with new values from incoming messages or discard attempted changes and deliver the original input to the next agent in the chain. This ensures that critical identifiers, references, and structured ISO 20022 data remain consistent throughout the payment lifecycle.

How TM Transforms Payment Architecture

Swift’s Transaction Manager does more than modernize messaging. It reshapes the entire architecture of cross-border payments by replacing fragmented, point-to-point exchanges with coordinated, state-based processing that ensures transaction integrity. This shift brings structural improvements that directly impact accuracy, speed, compliance, and operational efficiency.

Centralized Enforcement of ISO 20022 Standards

With TM, message validation is no longer based on stateless message syntax and dependent on each bank applying its own interpretation of the rules. This central network component now enforces business guidelines, and end-to-end transaction integrity as well. By the time a bank receives the transaction data, it is already clean, enriched, and aligned to the standard. This reduces message repair efforts and significantly improves straight-through processing rates.

Event-Driven Processing Instead of Message Chains

Traditional cross-border payments rely on a sequence of bilateral messages, with each institution independently validating and processing data as it moves through the chain. Transaction Manager does not replace this message-based model, but it introduces a centralized orchestration layer that processes in-scope messages consistently before they reach the next participant. This centralized processing reduces unnecessary data discrepancies, limits redundant follow-up communication, and improves alignment between participants, while preserving the underlying end-to-end payment flow.

Unified Visibility for All Participants

TM maintains one shared transaction record, and every bank involved can see the same information and the same sequence of state changes. No one works with partial updates or outdated data. This shared visibility eliminates the ambiguity that often slows investigations and enables faster root-cause identification when issues arise.

Consistent, Deterministic Processing Logic

Since all actions apply to a single authoritative transaction object, the outcomes of routing decisions, compliance checks, and validations become deterministic across institutions. This consistency reduces disputes, lowers operational risk, and leads to more predictable end-to-end payment experience across the network.

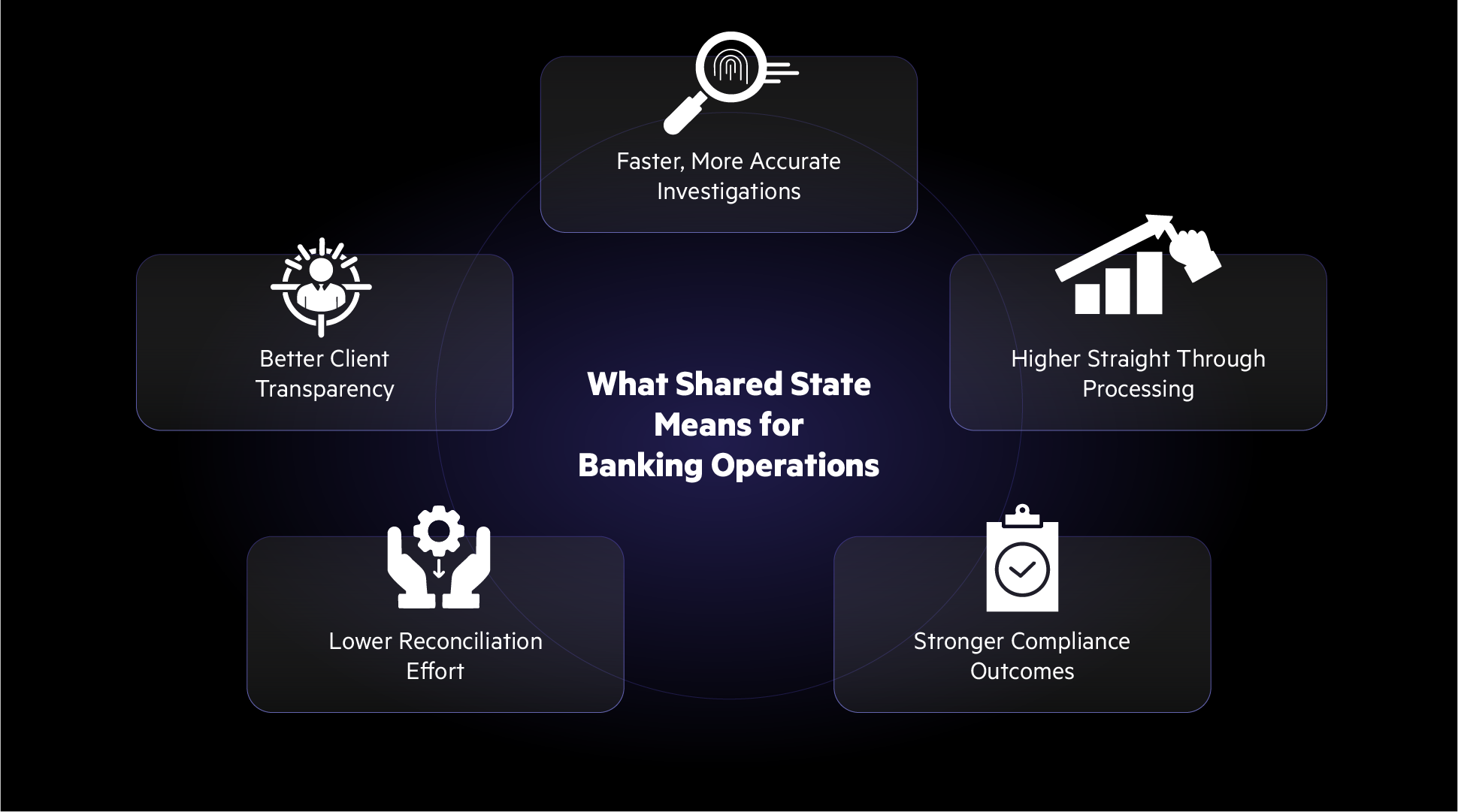

What Shared State Means for Banking Operations

Moving to shared state gives banks cleaner data, fewer breaks, faster investigations, and a more predictable payment experience.

1. Faster, More Accurate Investigations

One synchronized view of the entire payment lifecycle

No reconstruction from partial messages

Fewer false inquiries and quicker triage

2. Higher Straight Through Processing

Centralized integrity validation at the network level

Structured ISO 20022 data reduces repair points

Fewer manual interventions

3. Stronger Compliance Outcomes

All banks screen the same authoritative dataset

Higher quality AML and sanctions checks

Reduced variability in risk scoring

4. Lower Reconciliation Effort

Only one version of the payment exists

No comparison across multiple internal and external records

Network acts as the single source of truth

5. Better Client Transparency

Real-time visibility into every lifecycle event

Clear and consistent status updates

Fewer client queries and improved trust

Conclusion

Swift’s Transaction Manager (TM) represents a qualitative improvement for transactions on the Swift network, enhancing straight-through processing, reconciliations, and investigations. To fully leverage these improvements, banks must ensure that operational procedures and applications are aligned with TM’s stricter validation and central data integrity rules.

While TM strengthens payments via Swift, many cross-border transactions still originate from or pass through non-Swift networks. Therefore, it is crucial for payments and sanctions back-office teams to have tools that not only understand TM’s capabilities but also support investigations across domestic and other non-Swift networks, ensuring end-to-end visibility and operational efficiency.

.png)

.png)

.png)

.png)